Compound Interest Calculator: Your 2026 Planning Guide

Plan your 2026 investment growth with our compound interest calculator. Discover how to maximize your wealth and make informed financial decisions.

A compound interest calculator is defined as a tool that computes the future value of an investment by applying interest to both the initial principal and all accumulated interest over time. This exponential growth mechanism is the foundation of long-term wealth building. The standard formula is FV = P(1 + r/n)^(nt) + PMT × [((1 + r/n)^(nt) − 1) / (r/n)], where P is principal, r is the annual rate, n is compounding frequency, t is time in years, and PMT is the periodic contribution. Understanding each variable is what separates a useful projection from a misleading one. Investlytic's compound interest calculator is built around this exact framework, giving investors a structured way to model growth before committing capital.

What inputs do you need for a compound interest calculator?

A compound interest calculator requires five primary inputs: principal, recurring contribution, annual interest rate, investment duration, and compounding frequency. Each input carries distinct weight, and an error in any one of them shifts the projection materially.

The key inputs and their roles are:

- Principal. The starting balance. A $10,000 initial deposit behaves very differently from a $1,000 one, even at identical rates and time horizons.

- Recurring contribution. The amount added periodically, typically monthly. Consistent contributions often matter more than the starting balance over long time horizons.

- Annual interest rate vs. APY. The nominal rate is the base percentage. APY accounts for compounding and gives a more accurate picture of annual return. Always confirm which figure a calculator uses before trusting its output.

- Investment duration. Time is the most powerful variable. Compound interest creates exponential growth mainly after 15–20 years due to the repeated interest-on-interest effect.

- Compounding frequency. How often interest is calculated and added to the balance. Options typically include annually, quarterly, monthly, and daily.

Pro Tip: When entering an interest rate, verify whether the calculator uses the nominal rate or APY. Entering the wrong figure can overstate or understate your projected balance by thousands of dollars over a 30-year horizon.

How does compounding frequency affect your investment growth?

Compounding frequency is defined as how often earned interest is added back to the principal within a given year. The choice of frequency directly determines how much interest earns its own interest, and the differences are not trivial at the annual level.

| Compounding frequency | Periods per year | Relative impact on returns |

|---|---|---|

| Annually | 1 | Baseline |

| Quarterly | 4 | Moderate improvement over annual |

| Monthly | 12 | Significant improvement over annual |

| Daily | 365 | Marginal improvement over monthly |

The impact of compounding frequency shows diminishing returns at higher frequencies. Moving from annual to monthly compounding produces a meaningful jump in total returns. Moving from monthly to daily compounding, by contrast, produces a difference that is minimal for most retail investors over a single year. The practical implication is clear: prioritizing monthly compounding over annual compounding is worth the effort, but obsessing over daily versus monthly is not.

Consider a $50,000 investment at 7% for 20 years. Annual compounding produces a noticeably lower balance than monthly compounding. Daily compounding edges ahead of monthly, but the gap is small enough that it rarely justifies choosing one account over another on frequency alone.

Pro Tip: When modeling projections, use monthly compounding as your default assumption. It reflects the most common real-world structure for savings accounts and many investment vehicles, and it avoids overstating returns by assuming daily compounding that may not apply to your actual account.

How to apply the compound interest formula with contributions

The full formula, FV = P(1 + r/n)^(nt) + PMT × [((1 + r/n)^(nt) − 1) / (r/n)], handles both the growth of the initial principal and the accumulation of periodic contributions. The two components compound separately, which is why the formula has two distinct terms.

A concrete example makes this tangible. Investing $500 per month at 10% for 30 years produces a future value of approximately $1,131,857, with roughly $952,000 of that total coming from compounding alone. The total out-of-pocket contribution over 30 years is $180,000. The remaining $952,000 is pure interest on interest. That ratio illustrates why time and rate matter far more than the starting balance.

Contribution timing also shifts the outcome. Beginning-of-period contributions yield higher returns over 30–40 years because each payment starts compounding one full period earlier. The difference grows larger as the time horizon extends.

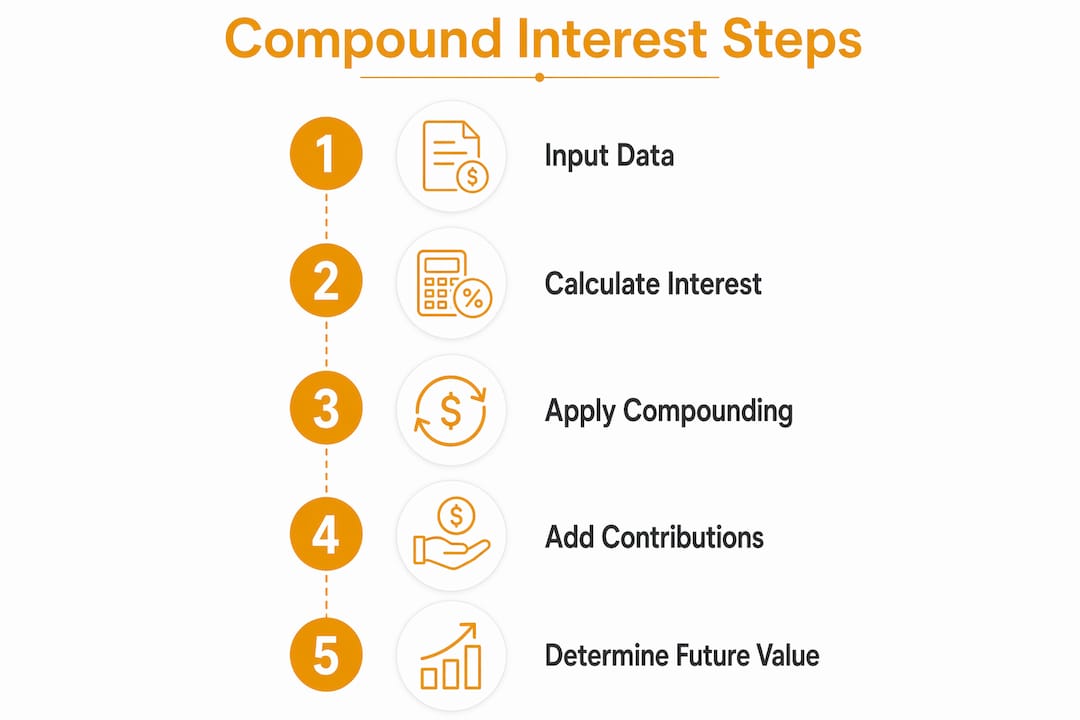

A step-by-step process for using the calculator effectively:

- Enter your starting principal. Use the actual balance you plan to invest today.

- Set your recurring contribution and frequency. Monthly is the most common and most realistic for salaried investors.

- Input the annual interest rate. Use a conservative historical average if you are modeling equity returns.

- Select compounding frequency. Monthly is the appropriate default for most scenarios.

- Set the investment duration in years. Run at least two scenarios: your target retirement age and five years earlier.

- Toggle between beginning and end of period. Compare the two outputs to see how much earlier contributions are worth over your time horizon.

- Read the output breakdown. A well-designed calculator separates total contributions from total interest earned, so you can see exactly how much growth came from compounding versus deposits.

The output breakdown is where most investors learn the most. Seeing that $952,000 of a $1.1 million balance came from compounding, not deposits, reframes how investors think about consistency and time.

What are common misconceptions when using compound interest calculators?

Calculator outputs are projections based on fixed assumptions, not guaranteed outcomes. Projected future value assumes a constant rate and ignores market volatility. Real investment returns fluctuate year to year, and a single bad decade can compress a 30-year projection significantly.

The most common pitfalls investors encounter:

- Confusing interest rate with APY. The nominal rate does not reflect compounding. APY does. Using the nominal rate in a calculator that expects APY inflates the projection.

- Ignoring inflation. $1 million in 30 years will be worth significantly less in today's purchasing power. A projection that does not adjust for inflation overstates the real value of the future balance.

- Assuming constant contributions. Life interrupts savings plans. Job changes, medical expenses, and market downturns all affect contribution consistency. A calculator assumes you contribute the same amount every period without exception.

- Treating the output as a guarantee. Users often mistake calculator projections for guarantees. Understanding the assumptions behind the projection is what makes the tool useful rather than misleading.

- Ignoring contribution timing. Choosing end-of-period contributions when your account actually processes them at the beginning of the period introduces a systematic underestimate.

Pro Tip: Look for a calculator that includes an inflation adjustment field. Entering a 2%–3% annual inflation rate converts the nominal future value into a real purchasing power figure, which is the number that actually matters for retirement planning.

How can you use a compound interest calculator to plan for long-term goals?

Long-term financial goals fall into three primary categories: retirement savings, education funding, and emergency reserves. Each category benefits from a different modeling approach, but all three rely on the same core calculation.

The Rule of 72 provides a fast mental check: divide 72 by the annual interest rate to estimate how many years it takes to double the investment. At 8%, money doubles in approximately 9 years. At 6%, it takes 12 years. This rule does not replace a full calculation, but it gives investors a quick sanity check when evaluating a rate of return.

Scenario comparison is where the calculator earns its value. Comparing different rates, contributions, and compounding frequencies helps investors visualize how small changes compound into large differences over decades. A $100 increase in monthly contribution at age 30 can add more to a retirement balance than a $500 increase at age 50, simply because of the additional years of compounding.

Practical applications for goal-based planning:

- Retirement. Model your target retirement age, then run a second scenario retiring five years earlier. The gap between the two outputs quantifies the cost of early retirement in concrete dollar terms. Investlytic's retirement planning calculator integrates compound interest projections directly into this framework.

- Education funding. Use a 529 plan contribution as the PMT input and the child's college start year as the duration. Compare scenarios with different annual contribution amounts to find the monthly savings target that meets the tuition goal.

- Emergency fund. Model a high-yield savings account with monthly contributions to determine how long it takes to reach three to six months of expenses. The emergency fund calculator on Investlytic handles this scenario directly.

Calculator results are a starting point, not a financial plan. Integrating projections with tax considerations, asset allocation, and income changes requires professional financial advice. The calculator tells you what the math says. A financial advisor tells you what the math means for your specific situation.

Key Takeaways

- Five inputs drive every projection: principal, contribution, rate, duration, and compounding frequency all affect the final balance materially.

- Monthly compounding is the practical standard: moving from annual to monthly compounding improves returns significantly; daily adds only marginal gains.

- Contribution timing changes outcomes: beginning-of-period contributions compound one full period longer, producing higher balances over 30-plus years.

- Inflation adjustments reveal real value: a nominal future value overstates purchasing power; always adjust for 2%–3% annual inflation in long-term projections.

- The Rule of 72 provides a fast check: divide 72 by the annual rate to estimate how many years it takes to double the investment.

Why I think most investors underuse their compound interest calculator

Most investors run one scenario, accept the number, and move on. That is the wrong approach. The real value of a calculator for compound interest is not the single output it produces. It is the comparison between five or six scenarios run back to back.

What I have found consistently is that investors underestimate the cost of waiting. Running the same inputs with a start date of today versus three years from now reveals a gap that is almost always larger than the investor expects. Compound interest creates exponential growth mainly after 15–20 years, which means the early years are precisely when starting matters most, even if the balance looks small.

The second mistake I see is ignoring inflation entirely. A $2 million projection 35 years from now sounds impressive until you adjust it for purchasing power. At 3% annual inflation, that $2 million is worth roughly $700,000 in today's dollars. That realization changes savings targets, contribution amounts, and sometimes career decisions.

My recommendation: use a calculator that separates total contributions from total interest earned, allows inflation adjustment, and lets you toggle contribution timing. Those three features alone eliminate the most common errors. Investlytic's compound interest tool includes all three, which is why I point investors there when they want a projection they can actually trust.

— Andrea

Investlytic's financial calculators for investment planning

Investlytic provides a full suite of financial calculators designed to move investors beyond single-scenario thinking. The compound interest calculator on the platform separates contributions from interest earned, supports inflation adjustment, and allows beginning-versus-end-of-period contribution toggling.

Beyond compound interest, the platform includes an investment return calculator, a retirement calculator, and a salary-to-investment tool that converts monthly income into long-term growth projections. For investors ready to act on their projections, Investlytic's broker comparison tool helps match the right investment platform to the strategy the calculator reveals. Over 10,000 active users rely on Investlytic for independent, unbiased analysis across all of these tools.

FAQ

What is a compound interest calculator?

A compound interest calculator is a tool that projects the future value of an investment by applying interest to both the principal and all previously earned interest. It requires five inputs: principal, contribution amount, interest rate, compounding frequency, and investment duration.

What is the difference between interest rate and APY?

The nominal interest rate is the base percentage before compounding is applied. APY, or Annual Percentage Yield, accounts for the compounding effect and reflects the true annual return, making it the more accurate figure for comparing investment options.

How does compounding frequency affect my returns?

Higher compounding frequency increases returns, but the gains diminish as frequency rises. The jump from annual to monthly compounding is significant; the difference between monthly and daily is minimal for most retail investors.

What is the Rule of 72?

The Rule of 72 estimates how long it takes to double an investment by dividing 72 by the annual interest rate. At 8%, the investment doubles in approximately 9 years.

Are compound interest calculator projections guaranteed?

No. Calculator outputs assume a constant rate and do not account for market volatility, inflation, or changes in contribution amounts. They are estimates designed to guide planning, not financial guarantees.

This article is for informational and educational purposes only and does not constitute financial advice. Always do your own research or consult a qualified financial advisor before making investment decisions.